白金級認可培訓資質(總部)

白金級認可培訓資質(總部)

課程試聽

課程試聽

職業(yè)規(guī)劃

職業(yè)規(guī)劃

ACCA中文教材

ACCA中文教材

考位預約

考位預約

免費資料

免費資料

題庫下載

題庫下載

模擬機考

模擬機考

CFA?成績查詢

CFA?成績查詢

GARP協(xié)會官方認可FRM?備考機構

GARP協(xié)會官方認可FRM?備考機構

-

在線咨詢

-

官方熱線

4008078199 -

APP下載

-

意見反饋

-

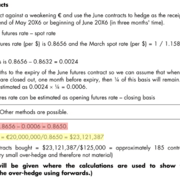

第56題 Lirio(b)Appendix 2: futures contracts

楊志鵬

發(fā)布于:2020-10-29 10:33:39

瀏覽376次  ACCA AFM

ACCA AFM

想問問老師,第56題 Lirio(b)Appendix 2: futures contracts。

(1) 答案“here this gives” 和“Expected receipt”的地方,直接用0.8656-0.0006. 這里用的是short cut 計算effective interest,(上課的時候說過這種做法不得分)。 所以我想用正常的做法。 但是基于我不知道 spot rate on the settlement date,所以我能不能假設spot rate on the settlement date 等同于 三個月以前的 june future rate = 0.8656,那么此時0.8656 + 0.0006 就是future rate on the settlement date?

(2) 答案在算number of contract的時候 使用的是用short cut計算出來的effective interest 折算成美元,再除上contract size。但是 這個地方為什么我們不使用June future rate (0.8656),來換算成美元呢?不知道這個是什么原理。

謝謝老師!

分享

名師解答

名師解答

user5dmtbr

發(fā)布于2020-10-30 09:32:10

user5dmtbr

發(fā)布于2020-10-30 09:32:10

使用10金幣查看此名師解答

我的金幣:0

提交成功

您的追加問題已提交成功

![]() 加載中...

加載中...

-

澤稷網(wǎng)校公眾號

-

澤稷網(wǎng)校微博

-

澤稷網(wǎng)校APP